Will S. Korea’s seaweed industry continue to grow?

The South Korean government wants its seafood exports to grow by 50% in the next 5 years. On the back of the recent surge in popularity of gim (nori / Porphyra) and abalone, the country aims to go from a record-breaking 3.15 billion dollars export in 2022 to a record-shattering 4.7 billion dollars in 2027.

Will this happen?

Before tearing into the details, let’s ask ourselves why South Korea became a prolific seaweed producer in the first place. Yes, seaweeds are a traditional part of Korean cuisine, but moules-frites is Belgium’s national dish and yet my country does not cultivate any mussels.

Instead, all it takes is a train ride from Seoul to Busan for (part of) the answer to present itself in full view. There is little arable land. It’s all hills. Food self-sufficiency in S. Korea is the lowest in the OECD, and arable land keeps declining at 1-2% per year. The lack of farmland made expansion into the sea an obvious strategy.

I use the word strategy on purpose, because growing the seaweed industry in Korea was, and as the opening sentence reveals, continues to be, a top-down, strategic choice; initiated, enabled and sustained by the government, in partnership with producers and processors.

Supply: negative signals

Climate change

Climate change is growers’ chief concern. Higher water temperatures weaken growth and resilience and shorten the growing season. The nori doesn’t grow as big as it used to, and processors complain their nori sheets have become more brittle.

On top of that, severe droughts see less nutrients washing into the sea from the rivers, adding to growth issues. There is a risk that fresh water to wash the seaweeds will run out.

Labor shortages

As I exited the bus station of the country’s seaweed capital Wando, I was shouted at in Russian. Did I need a job? No, I didn’t, but others did. The waitress was from Kazakhstan, the cleaning lady from Cambodia. The farm hands were East Timorese.

At first sight, South Korea seems to have a more pragmatic approach towards labor migration compared to its Japanese neighbors. Even if they are often treated cruelly and left to linger in illegality, the government does let in hundreds of thousands of foreign workers. But that’s not enough. Large labor shortages remain. And only 19% of Koreans support an increase in immigration.

Young Koreans don’t want to farm. In 2020, the average South Korean farmer was 66 years old. As Korean women continue their birth strike and the world’s lowest birth rate drops even lower (0.59 in Seoul last year), society faces a reckoning. South Koreans need to address their racist attitudes. If they don’t, their (seaweed) economy might suffer.

Supply: positive signals

More cultivars

The government’s Golden Seed project is bearing fruit - more cultivars are being registered in an effort to balance resilience, productivity and taste. The focus is clearly on Pyropia (gim/nori).

If Covid taught us anything, it’s that the South Korean government is run by capable people. It’s the OECD government most likely to listen to its people. As the introduction showed, the government is keen to continue its support and nurture seaweeds to become the semiconductor of the food industry.

Species variety

Something I did not fully appreciate until I visited the country, is the variety of species grown and eaten in Korea. Sure, we all know gim (Pyropia / nori), dasima (Saccharina / sugar kelp), parae (Ulva / sea lettuce), tot (Sargassum / hijiki) and miyeok (Undaria / wakame), but what about maesaengi (Capsosiphon fulvescens), cheonggak (Codium fragile), gompi (Ecklonia stolonifera) or pulgasari (Gloiopeltis tenax)?

All of these and more are used in a variety of dishes, their diversity adding resilience as the industry faces down climate pressures and market shocks.

Is a lack of space to expand an issue? It isn’t something I heard. One farmer said they could increase wakame production 5x if the demand was there. Statistics show that productivity has grown in recent decades even if the area under cultivation has remained constant. But according to others, this is a frequently-cited complaint for growers.

Price signals are also mixed. The price of gim has shot up in the past year because of shrinking supply, and this seems to be affecting consumer preferences.

At the same time, the price of wakame has remained bolted to 80$/ton.

Demand: negative signals

Korean diets are changing. Less rice, more meat.

Does that mean that Koreans’ love for seaweed is flagging? Actually, no. Between 2014 and 2021, daily seaweed intake did not budge: some 3.5 g in salads and snacks, and 21 g in soups and broths.

I was told the sushi hype is over. I don’t see that either, though. Maybe there is a bit of oversupply in Paris and LA after record take-out sales during Covid. But there are still a lot of unbuilt sushi restaurants in the world’s emerging markets. If I was selling sushi, I would be more worried about securing fish than customers.

What could become an issue in future is that, according to one food safety expert, Korea will struggle to comply with EU regulations for heavy metal and iodine levels, cadmium in particular. Perhaps some of those within-limits Korean lab tests I was shown would have different outcomes if retested in Germany (it is curious how many S. Korean exporters ship to Poland…is there a big Asian community? Are Polish people the culinary adventurers I did not know they were? Or is the customs department a bit more relaxed compared to Germany?).

Will this ultimately have a big effect on Korea’s export chances? On the one hand, while there seems to be some progress made on heavy metal removal, there is still a lot we don’t know.

On the other hand, Koreans are eating their own stuff and, while there is some contamination, they seem to be doing fine. Korean food companies are also establishing more production facilities abroad to shorten the supply chain, be closer to the target market and reduce the burden of customs and food safety regulations.

Demand: positive signals

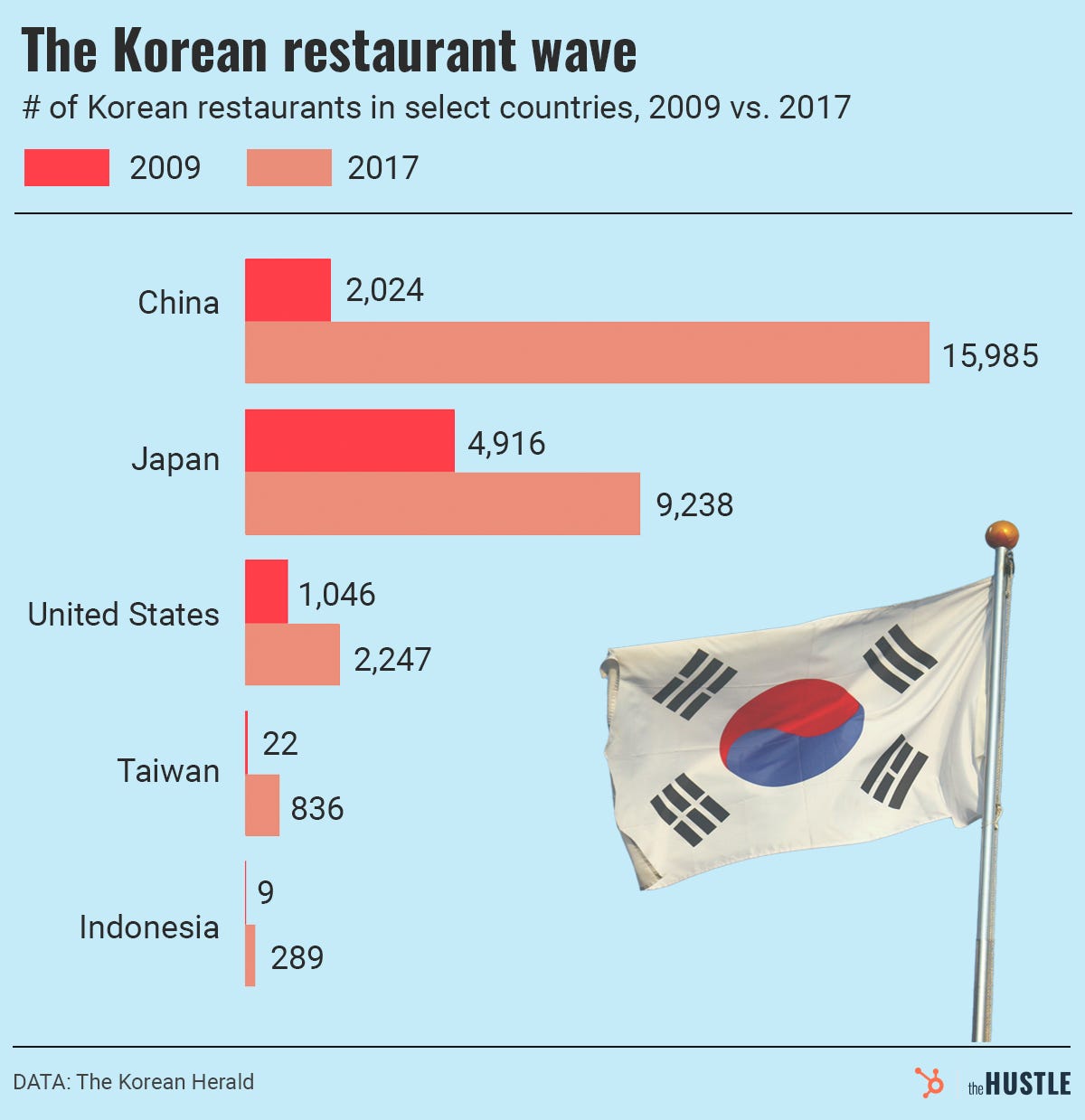

While the rest of the world is starting to get a taste for Korean seaweeds, the biggest market for Korean gim remains Japan. The worst harvest in more than 50 years means Japan is now 2.5 billion nori sheets short of its yearly consumption. While you would not want to call that “positive” news, the continued decline of Japanese seaweed production opens up more market share for S. Korea.

China’s harvest numbers are more difficult to gauge but anecdotal evidence seems to suggest an increasing shortfall as well.

Beyond nori, some 70% of Korea’s kelp harvest is used or sold as abalone feed, and the growth of the Korean seaweed industry is closely linked to the growth of its abalone aquaculture. While the abalone market does fluctuate, it has proven resilient over time.

Finally, Korea’s gastrodiplomacy efforts are set for another round of investment. Latest country to fall for its flavors: India.

Investment & innovation: negative signals

Not much has happened in terms of product innovation in the past few decades. At the recent Seoul Seafood show I saw ultra-low-calorie kelp noodles, seaweed soy milk and a plastic-free seaweed facial mask, but mainly just a lot of gim, roasted, toasted and flavored.

New technology to alleviate labor shortages and improve first-step processing: maybe people are out there inventing it, but I did not find them. Even the well-established nori sheet factories felt crowded to me compared to the average food processing plant featured on Discovery Channel.

Investment & innovation: positive signals

Botamedi has been researching Ecklonia cava since 2001. It gets a lot of mileage out of its flagship Seanol molecule, the first dietary marine polyphenol approved by the American FDA. Products include cosmetics, dietary supplements, a pharmaceutical pipeline and even an anti-snoring spray.

Earlier this year, Botamedi raised a 600 million euros Series B round from European asset managers. This on top of $159 million from China in 2018. Beyond biotech, several food companies I recently visited were investing in new factories, like Wandomom, who built a new $2.3 million facility in 2021.

Korean seaweed companies are also being offered favorable opportunities to invest abroad, for instance in Indonesia’s Natuna region.

Conclusion

South Korea is on a 70-year winning streak that is showing few signs of ending. Per capita income in 1955 was lower than that of Haiti or Yemen and most people barely made it into their 40s. Soon, Koreans will take Japan’s crown of longest-living people in the world, and the country is now the 10th-biggest economy and the 6th-biggest exporter in the world.

On the flipside, S. Korea has the highest suicide rate and the biggest gender pay gap in OECD, and the most alcoholics in the world. Koreans spend more on luxury brands than anyone else.

Maybe more is no longer better?

Yet absolutely no one I met on my trip to Korea said “we’re doing fine, it’s enough now.“ All were hungry for more sales abroad. No one asked if the Korean seafood economy really still needs to grow, and if so, by how much. Why 50%?

Anyway. Here’s how I see it: while demand for Korean seaweeds as food and feed is set to continue to rise, the work on cultivars and automation might not move quick enough to offset the negative effects of climate change and labor shortages in the near term, leading to a shortage of supply and higher prices.

This in turn could spur innovation and a search for new geographies.